Summarize with AI

The opening of gas markets in France

Mis à jour le

March 6, 2026

7

Min reading

This year, you may have received a bit of strange mail. A letter announcing the end of regulated gas tariffs! This is the case for millions of individual customers. In fact, liberalization of gas markets continues to develop.

As far as professional customers are concerned, the market has been completely liberalized since the 2000s. This trend continues to change the economic landscape of energy in France.

Regulated tariffs are often a subject of discord with the European Union. These are rates decided by the State on the proposal of the CRE (Energy Regulatory Commission). This therefore goes against the principles of a liberalized market wanted by Europe. That is why all offers administered by the State are gradually being phased out.

The French gas market has undergone numerous changes. Indeed, it went from total nationalization to gradual openness in the 2000s. Businesses for which the cost of gas is a crucial factor are used to negotiating their contracts. Gradually, these principles are spreading throughout the French economic landscape.

We will therefore see what were the stages in the opening of gas markets in France. In this way, we will be able to understand the current energy challenges. It will also be an opportunity to take stock of the opening of markets in 2021.

Indeed, it is not uncommon to hear criticisms against this liberalization. Some opinions judge these developments severely and question their economic efficiency. It is by understanding the origins of European directives and their implementation that you can form your own opinion. If you want to know more about the subject, we invite you to continue this article!

The different stages of the opening of gas markets

Changes in the energy sector in the 20thE century

First of all, it is important to give a historical overview of the energy markets in the 20E century.

To explain The opening of markets, first of all, we must describe the wave of post-war French nationalization. The Second World War highlighted the strategic importance of the energy sector. For this reason, once in place, the new government decided to nationalize the vast majority of companies in the sector.

The companies EDF and GDF were therefore created in April 1946.

Thus, for nearly half a century, GDF was in a situation of monopoly on all gas activities: from production, long-term gas purchases, to transport and finally supply. From upstream to downstream, the entire gas market chain is managed by the same state-owned company.

The first steps in liberalizing gas markets

Because of its membership in the European Union, France is committed to translating European directives into French law. The EU is committed to creating a single energy market across Europe. To do this, the state monopolies of the various countries must be abolished and free competition established. In any case, this is the economic point of view adopted by the European authorities.

It was therefore in 1998 that the Directive on natural gas markets appeared. The aim is to gradually open up all sectors of activity to free competition, from production to energy supply. However, transport and delivery activities remain in a monopoly situation.

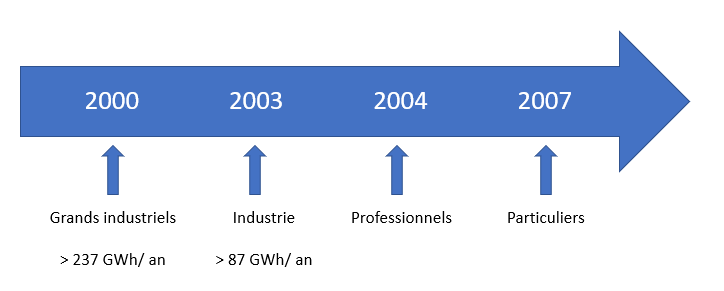

First of all, we saw the gradual opening up of various customer segments during the 2000s.

That is to say, on these dates, customers were authorized to take out a contract with a alternative supplier. Today, this is the case for all French consumers.

Continued liberalization and unification of European gas markets

Now, French customers have a choice. However, with the European directive 2009/73/CE and its transcription into French law, things will accelerate.

Europe then decided to create a unified internal gas market. The situations were very heterogeneous at that time. Some countries, such as the United Kingdom, have already initiated the opening of markets, unlike others in a monopoly situation.

The founding principles of the markets that we know today are emerging. Transparent and non-discriminatory access to the gas network is established. There is freedom of establishment for all producers, and of choice of supplier for customers.

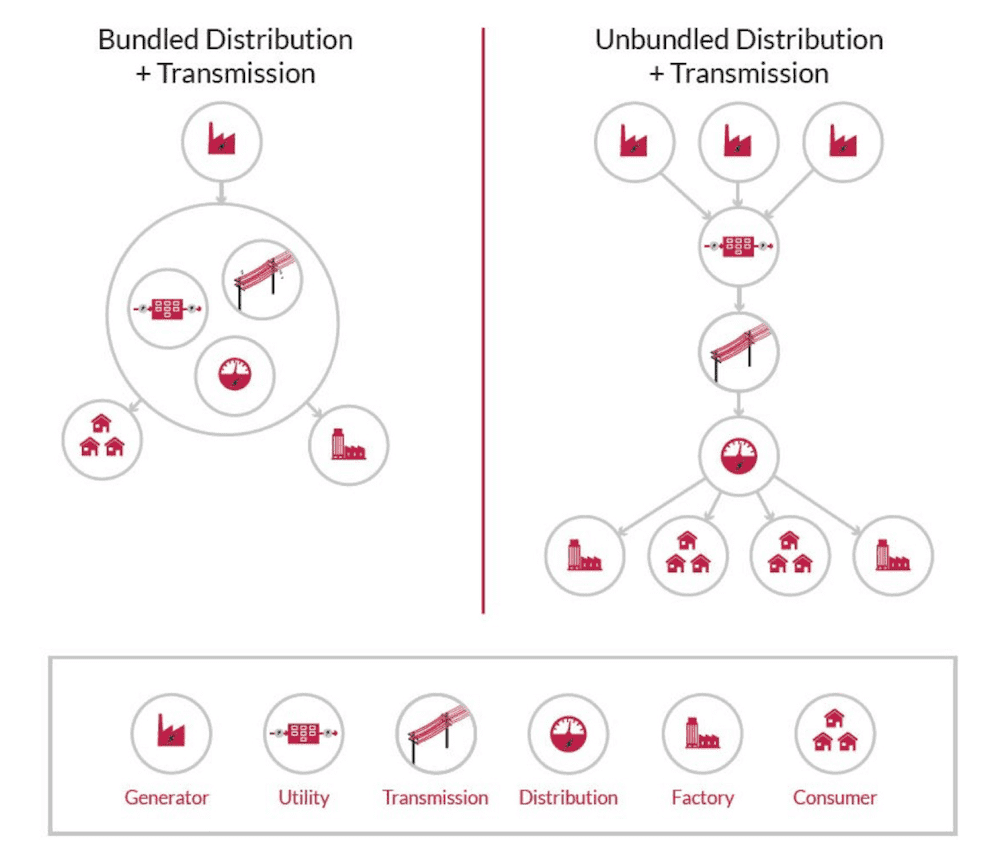

The European Union wants no player to have too much of a competitive advantage. For this reason, supply, distribution and production activities are clearly separated. This is what is commonly called” The unbundling ”.

Source: ALSF Academy

As you can see, in this diagram (on the right), networks are always unique. However, there are a multitude of actors up and down stream.

In France, network management activities remain under the monopoly of GRTgaz, Teréga as well as GRDF.

Then there is Three dates important things to remember:

- June 19, 2014 : regulated sales tariffs (TRV) are abolished for very large gas consumers.

- 1Er January 2015 : TRVs disappear for sites whose consumption is > 200 MWh/year.

- 1Er January 2016 : finally, this concerns non-residential consumption sites > 30 MWh/year as well as condominiums > 150 MWh/year.

It is therefore interesting to note that there was a first phase of market opening, followed by a second phase of elimination of regulated tariffs.

This second phase is still continuing at present with the retail market.

What is the balance sheet for the opening of gas markets in France?

It is not uncommon to read or hear some very severe opinions about the opening of markets. Indeed, competitive tendering was supposed to have certain repercussions, such as a drop in gas prices. However, the evolution of supply prices does not depend only on the economic structure of the sector, but on many other parameters.

So what is the result of the opening of markets? This is a delicate question to which we will try to provide some answers.

First, a few key reminders. In France, the gas market represents nearly 11.5 million sites with an annual consumption of 485 TWh.

In terms of the number of sites, 94% of the gas market is made up of residential sites, as you can see. However, they represent only 25% of the volumes consumed.

The opening of markets has prompted the majority of French consumers to take an interest in market offers. The situations are very different between the private sector and the professional sector.

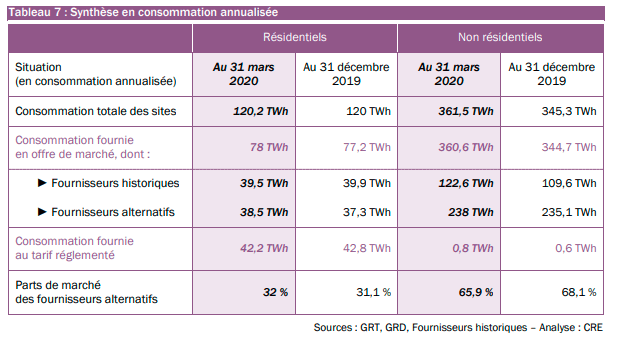

This table gives us a lot of answers; we have chosen to select two of them:

- For individuals, even with the existence of regulated tariffs, more than 70% of consumption is affected by market offers.

- For professionals, it is normal to find a rate close to 100%. However, it is interesting to note that the share of alternative suppliers represents nearly 65% of total consumption.

We can therefore see that the opening of markets has allowed the emergence of sustainable competitors over time. This is one of the expected effects of these large-scale economic developments. Indeed, competition is supposed to be synonymous with lower prices. According to the principles of the liberal economy, pure and perfect competition stimulates competitors and pushes them to improve the services offered.

The end consumer is therefore supposed to be the big winner in this competitive process.

In practice, this is not that easy. The emergence of new players may be hampered by the dominant position of former state-owned enterprises. However, it should be noted that a certain number of new offers have emerged. In addition, gas market players are encouraged to constantly improve their customer services.

Indeed, even recently, The National Energy Ombudsman highlighted some practices in the gas and electricity supply sector.

What are the consequences for prices?

As we can see, regulated gas sales rates increased by €1.1/MWh between 2008 and 2020, which is relatively low over such a long period of time.

These rates are supposed to cover all the costs of historical suppliers. So they cover among other things long-term gas purchases on wholesale markets (the gas exchange). Changes in market prices depend on several factors, such as:

- the price of oil (up to a certain extent),

- gas demand,

- the temperature,

- shale gas production,

- geopolitical tensions.

The causes of price variations are therefore multiple and heterogeneous. This shows that it is difficult to say that only the liberalization of the sector affects prices in general.

In summary, trying to link gas prices to the liberalization of the sector is an extremely complex exercise if you want to be precise. It is difficult to define the precise causes of certain movements.

For example, we can mention one of the largest European hubs: the TTF index. Located in the Netherlands, this market place experienced variations sometimes linked to the price of oil, then these two indices were uncorrelated. This example shows how complex it is to explain price movements with explanations that are too hasty.

In any event, contrary to some opinions in the press, the liberalization of the gas sector did not lead to an increase in prices. These have been relatively stable, especially since the 2017 oil price drop. However, it can be seen that, as wanted by the EU, these developments have allowed the creation of real competition on the gas market.

Take the first step towards optimization

In a few clicks, organize an exchange with one of our experts.

weekly newsletter subscribers

4.9

The answers to your questions

Pourquoi ma facture de gaz va-t-elle augmenter en 2026 ?

L'augmentation s'explique par la revalorisation de l'Accise sur le gaz à 16,39 €/MWh et la hausse de 3,41 % du tarif de transport (ATRT 8).

S'y ajoute l'entrée en vigueur des Certificats de Production de Biogaz (CPB), un nouveau coût réglementaire pour soutenir le biométhane.

Face à ces évolutions, Sirenergies vous accompagne dans l'achat de gaz naturel pour sécuriser vos prix malgré la volatilité du marché.

What is the Multiannual Energy Programming (PPE)?

La Multiannual Energy Programming (PPE) is the strategic management tool for France's energy policy. Established by the 2015 law on energy transition for green growth (LTECV), it serves as a compass for the State, communities and businesses.

Concretely, the PPE sets the priorities for action of the public authorities for the management of all forms of energy on the national territory. It covers a period of ten years, divided into two periods of five years, and must be revised periodically to adapt to technological and economic developments.

It deals with major topics such as:

- Security of supply.

- Improving energy efficiency and reducing consumption.

- The development of renewable and recovered energies.

- The electrical production strategy (nuclear, thermal, etc.).

- The balanced development of networks and storage.

It is crucial not to confuse it with National Low Carbon Strategy (SNBC). While SNBC sets carbon budgets (the ceilings for greenhouse gas emissions by sector), the PPE determines the technical and energy resources to achieve them.

Quelle est la différence entre un prix Forward et un prix Spot ?

Le prix Forward est fixé à l'avance (sécurité budgétaire), tandis que le prix Spot varie heure par heure selon le marché (opportunité mais risque élevé).

Quel sera l'impact réel du VNU sur ma facture d'électricité professionnelle ?

L'impact dépendra des prix de marché. Le mécanisme prévoit une redistribution si les prix dépassent 78 €/MWh. Cependant, si les cours restent bas (actuellement autour de 60 €/MWh), le dispositif ne s'activera pas. La facture sera alors indexée à 100% sur les prix de marché, rendant le choix du fournisseur et du moment d'achat critiques.

Qu'est-ce que le dispositif VNU qui remplace l'ARENH en 2026 ?

La Vente de Nucléaire Universelle (VNU) est le nouveau mécanisme de régulation des prix de l'électricité en France. Contrairement à l'ARENH, il ne s'agit plus d'un volume fixe à prix réduit, mais d'une redistribution financière des revenus excédentaires d'EDF aux consommateurs, basée sur les prix de marché et les coûts de production du nucléaire historique.

Pourquoi l'IA ne peut-elle pas prédire le prix de l'énergie avec exactitude ?

Car les marchés dépendent de facteurs exogènes imprévisibles (géopolitique, météo soudaine, politique) que les modèles basés sur l'historique ne peuvent pas anticiper, tout comme on ne prédit pas le Loto.

Fin de l'ARENH au 31 décembre 2025 : comment sécuriser mon budget énergie pour 2026?

La fin de l'ARENH (Accès Régulé à l'Électricité Nucléaire Historique) marque l'arrêt de la fourniture d'électricité à prix fixe garanti (42 €/MWh).

Dès le 1er janvier 2026, les entreprises sont exposées aux prix de marché, mais deux nouveaux mécanismes de régulation prennent le relais, bien que leur logique soit différente :

- Le Versement Nucléaire Universel (VNU) : Ce n'est pas un tarif d'achat, mais un mécanisme de redistribution a posteriori. Si les prix de marché de l'électricité nucléaire dépassent un certain seuil (environ 78 €/MWh selon les estimations pour 2026), EDF reversera 50 % des revenus excédentaires aux consommateurs. Attention : Si les prix de marché restent modérés (sous les 78 €/MWh), le VNU ne se déclenche pas. Il agit comme une assurance contre les flambées extrêmes, pas comme un tarif bas garanti.

- Les CAPN (Contrats d'Allocation de Production Nucléaire) : Réservés aux industriels électro-intensifs, ces contrats de long terme (10-15 ans) permettent de réserver une part de la production nucléaire en échange d'une participation aux coûts du parc. Ils offrent une visibilité sur le long terme pour 50 à 70 % des volumes consommés.

Conseil stratégique : Ne comptez pas sur le VNU pour réduire votre facture en 2026 si les marchés restent stables. Auditez vos contrats dès maintenant pour intégrer une part de prix fixe ou explorer des "Power Purchase Agreements" (PPA) pour sécuriser vos coûts sur le long terme.

Mon entreprise peut-elle tirer profit des nouvelles Heures Creuses (11h-17h)?

Absolument. La réforme des heures creuses vise à absorber la surproduction solaire en milieu de journée. Les créneaux d'heures creuses se déplacent progressivement vers la plage 11h00 – 17h00, notamment en été. C'est une opportunité majeure pour les sites industriels ou tertiaires capables de flexibilité.

Conseil stratégique :

- Pilotage de la charge : Si vous avez des processus énergivores (fours, broyeurs, recharge de flotte de véhicules électriques, production de froid), déplacez leur fonctionnement sur la pause méridienne. L'électricité y sera moins chère et moins carbonée.

- Autoconsommation : C'est le moment idéal pour coupler cette tarification avec une installation photovoltaïque en toiture ou en ombrière de parking. Vous effacez votre consommation réseau au moment où le tarif serait le plus avantageux, ou vous profitez des prix bas du réseau si votre production ne suffit pas.

What are the electricity offers offered by bellenergie Business?

The range E @sy is available in four pricing structures to adapt to each risk profile:

- E @sy Fixed: 100% budget visibility without variation.

- E @sy Click: Smoothed price thanks to staggered purchases on the markets.

- E @sy Block + Spot: A mix between a secure base and a portion indexed to daily prices.

- E @sy Sport: A 100% dynamic offer to take advantage of downside opportunities in real time.

Quels sont les cas d'usage concrets des différents types d'IA pour un acheteur d'énergie ?

Chaque modèle d'IA répond à un besoin spécifique du cycle d'achat :

- L’IA générative sert d'assistant de recherche pour synthétiser en quelques minutes des rapports de marché massifs (veille stratégique).

- L’IA déterministe est l'outil de la fiabilité : elle est indispensable pour le forecast (prévision de consommation) car ses calculs sont mathématiques et reproductibles.

- L’IA probabiliste est dédiée à la gestion des risques : elle simule des scénarios (ex: météo, stocks) pour quantifier l'incertitude sur les budgets futurs.

L'expertise humaine reste néanmoins indispensable.

What are the customer reviews on bellenergie Business's customer service?

In 2025, the supplier had a NPS (Net Promoter Score) of +16 and a note of 4,17/5.

Satisfaction is based on a “zero solicitation” model and 100% in-house customer service in Toulon, guaranteeing proximity and responsiveness that cannot be found with major historical suppliers.

What is the main objective of the Multiannual Energy 3 Programming?

The central objective of PPE 3 is to engage France towards carbon neutrality by 2050 by breaking the country's historical dependence on fossil fuels.

Today, approximately 60% of final energy consumption in France still relies on imported oil and natural gas. PPE 3 aims to radically reverse this trend by setting an ambitious target: to reach 60% of carbon-free energies in final consumption by 2030.

To achieve this, PPE 3 pursues three major sub-objectives:

- Massive decarbonization: Replace fossil fuels with low-carbon electricity or renewable heat in industry, transport and buildings.

- Energy sovereignty: Reduce the national energy bill (around 60 billion euros per year) and get rid of the volatility of the global gas and oil markets.

- Economic competitiveness: Guarantee businesses and households access to stable, abundant and predictable energy at a predictable cost, disconnected from geopolitical crises.

Pourquoi le mécanisme de capacité a-t-il été créé ?

Instauré en 2017, ce dispositif répond à un enjeu de sécurité nationale.

L'électricité ne se stockant pas à grande échelle, le réseau doit être capable de répondre instantanément à la demande, même lors des pics de froid hivernaux. Le mécanisme incite financièrement les producteurs à maintenir leurs centrales disponibles et les entreprises à réduire leur consommation (effacement) lors de ces périodes critiques.

L'IA remplace-t-elle les analystes en énergie ?

Non. L'IA traite la donnée (data processing), mais l'analyste apporte la compréhension du contexte (market sentiment) et la prise de décision stratégique.

Pourquoi le seuil de 78 €/MWh est-il critiqué par les experts ?

Ce seuil est jugé élevé par rapport aux prévisions actuelles du marché. Si le prix de l'électricité reste en dessous de 78 €/MWh, les entreprises ne bénéficieront d'aucune redistribution. Cela signifie que la protection promise par la réforme pourrait être inexistante dans un marché baissier, d'où l'importance de stratégies de sourcing agiles et d'outils de monitoring comme Pilott.

The answers to your questions

No items found.